The postal and delivery sector generated around EUR 110 billion in revenue in 2021 (0,8 per cent of total GDP) and employed around 1.5 million people (0.7 per cent of total employment in EU-27) across the EU-27 Member States.

Two opposing dynamics in the letter and parcel delivery markets are continuing to cause fundamental challenges for postal market stakeholders:

As a result of these developments, policymakers also face challenges as they aim to ensure a financially and environmentally sustainable Universal Service Obligation while preserving a basic, affordable service level for all users. Along with the evolution of technology, business models and trends within the postal sector, policymakers face important trade-offs when adapting current regulations to ensure that user needs are covered accordingly.

This study presents, describes, and assesses the most important evolutions in the letter and parcel delivery markets in the 27 Member States of the European Union, in the United Kingdom, and in the EFTA countries of Iceland, Liechtenstein, Norway, and Switzerland in 2017-2021 taking into consideration the impact of the covid-19 pandemic and other relevant external events on the postal sector. It also outlines the most significant evolutions of the regulatory framework in the Member States.

The report is structured around seven chapters, providing insights on:

The substitution of letter mail for electronic alternatives continues to drive letter mail volumes down. In the 2017 to 2021 time period, letter mail volumes declined by on average 6.1 percent per year, compared to 4.3 percent per year 2013 to 2017.

In an industry heavily characterised by large economies of scale, this development causes the cost per item delivered to increase substantially. To cope with such cost increases, many European universal service providers (USPs) have increased prices and forced further cost reductions throughout their businesses to ensure the financial sustainability of their letter delivery business.

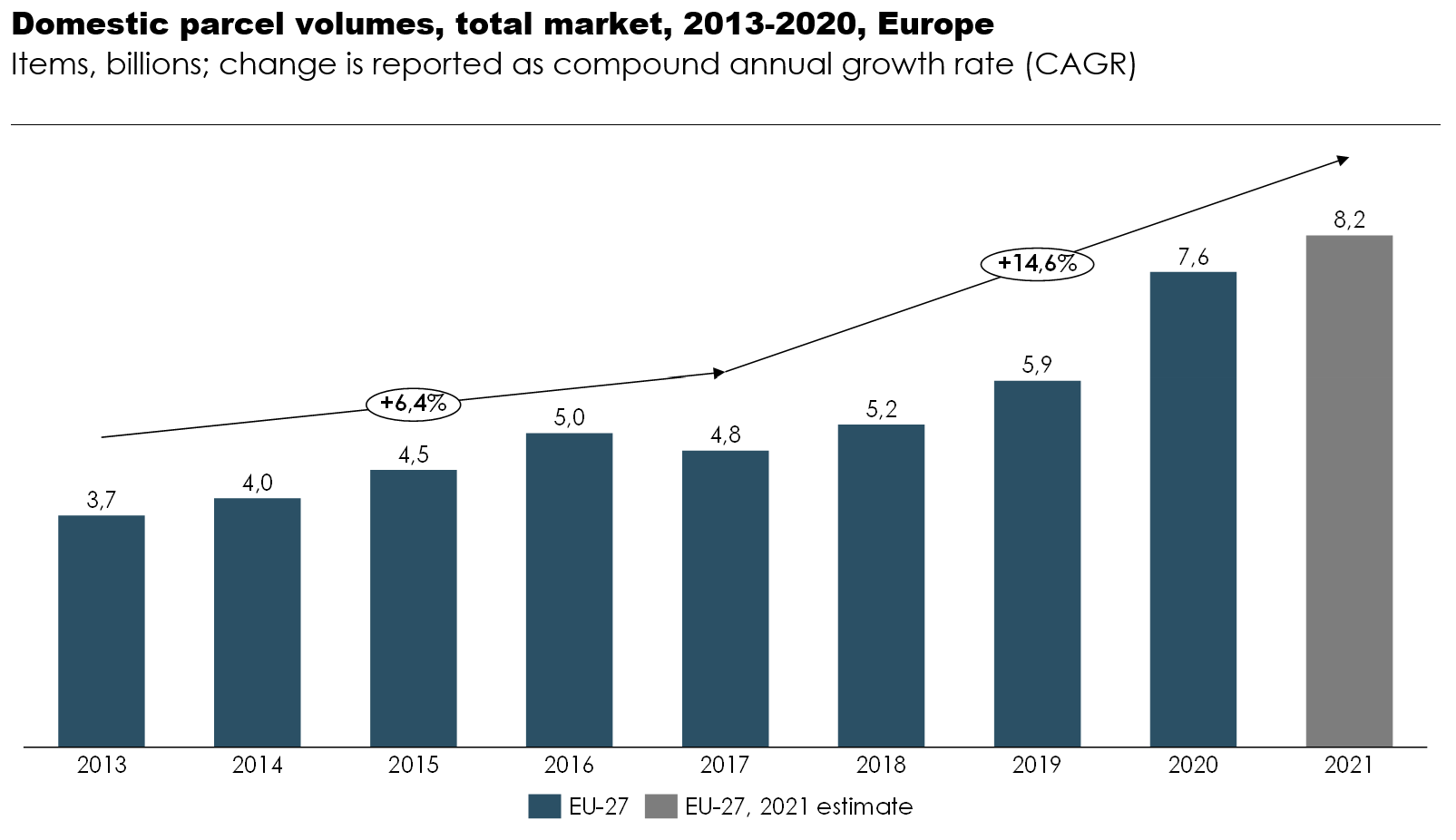

The situation looks very different for parcel delivery. An increase in e-commerce, accentuated by the covid-19 pandemic, has further boosted competition in the courier, express and parcel (CEP) market. Between 2017 and 2021, domestic parcel volumes increased by 14.6 percent annually, up from an annual increase of 6.4 percent in 2013-2017.

As a result, new players have entered the market at different levels of the parcel delivery value chain and we observe new business models being developed to compete with traditional postal operators, specifically in relation to last-mile delivery.

Developments in the universal service

The growing importance of parcel deliveries and the declining importance of letter mail for consumers as well as for businesses across Europe raises a question of whether there is a need to revise the postal USO – both at the EU level and in individual Member States. Between 2017 and 2021, Member States such as Belgium, Denmark, Finland, Norway and Sweden have adjusted their minimum USO requirements, particularly in terms of delivery frequency and delivery speed, to accommodate the changing dynamics in the postal sector. Some countries (e.g., Ireland and Sweden) have also made changes in postal sector price regulation.

Adjustments to the USO can have significant financial benefits as they may remove part of the so-called net cost of the USO. They need, however, to be carefully weighed against their impact on users and the benefits derived from the current USO specification.

Environmental impact

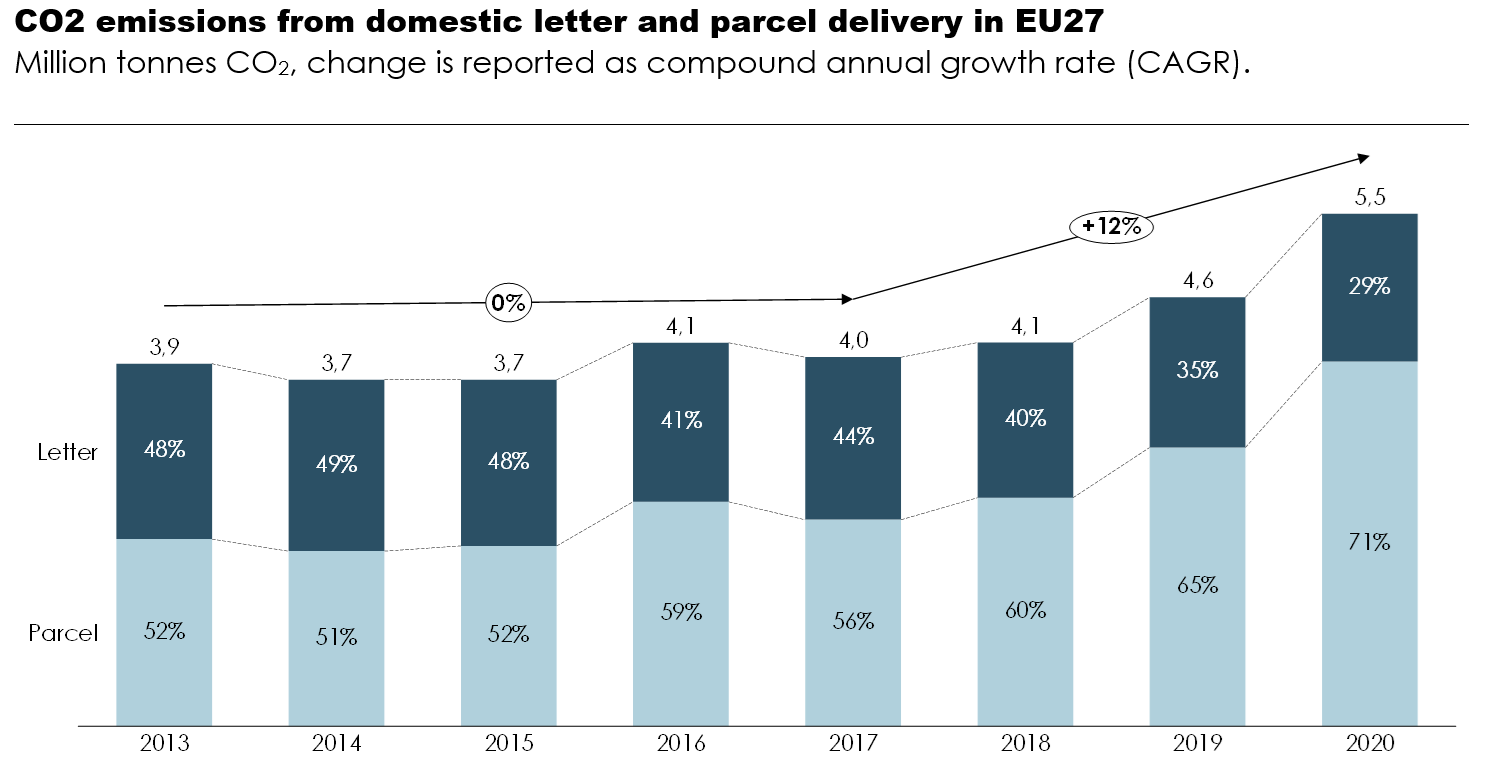

Booming e-commerce volumes have increased the environmental footprint of the EU postal sector between 2017 and 2021. Whereas CO2 emissions from domestic letter mail and parcel deliveries in the EU were relatively constant between 2013 and 2016, from 2017 total emissions increased by an average of 12 per cent annually. This shift is not only a result of more parcels being delivered. It is also due to the fact that the Co2 impact per parcel started to increase in 2018 after having declined consistently for several years.

We conclude that despite significant efforts and investments in green solutions undertaken by industry players, growing parcel delivery volumes will continue to create challenges for postal operators to reduce their environmental footprint. Hence, a true green transition of the postal and delivery sector depends on the broad involvement of all players driving the change in this industry.

Figure 1: CE Survey of NRAs. Copenhagen Economics (2018) Main Developments in the Postal Sector 2013-2016. European Commission, DG GROW Postal Statistics Database.

Figure 2: EC Growth postal database; CE Survey of NRAs; Copenhagen Economics (2018) Main Developments in the Postal Sector 2013-2016. Data for the UK for 2016-2020 was gathered from Ofcom’s yearly financial reports on the postal market.

Figure 3: Copenhagen Economics estimation based on national market volume data and emission estimates from IPC.

Download